Audit analytics on supplier payments: Bristol supplier spend review

This project analyzes public supplier payment data from Bristol City Council to build an audit analytics workflow around supplier spend, repeated payment patterns, and risk-based review.

The dataset includes three monthly files of payments over £500 and is especially useful for an accounting and audit-focused project because it contains fields such as supplier name, amount, payment date, transaction number, and spending category descriptions.

Source: data.gov.uk — Local authority spend over £500: Bristol City Council

Repository: github.com/FlaviaRossi/data-projects/tree/main/bristol-supplier-spend

Dataset scope

After cleaning malformed and out-of-period rows, the working dataset includes:

- 17,959 payment rows

- 3 months of data

- 1,900 suppliers

- 14,698 transaction numbers

- £189.5M in total analyzed spend

What the review focused on

The analysis was designed around a set of useful audit questions:

- Which suppliers concentrate the largest share of total spend?

- Which spending categories dominate the dataset?

- Which repeated payment patterns should be reviewed?

- Which transactions look unusual relative to each supplier’s normal behavior?

- Can an explainable risk score help prioritize review work?

1. Spend concentration by supplier

Supplier concentration is one of the clearest starting points in a review like this.

Key findings:

- the top 10 suppliers account for about 21.96% of total spend

- the top 25 suppliers account for about 35.25% of total spend

This is useful because concentration risk often matters even when individual transactions are valid. A small number of suppliers can drive a large share of exposure, operational dependence, or review effort.

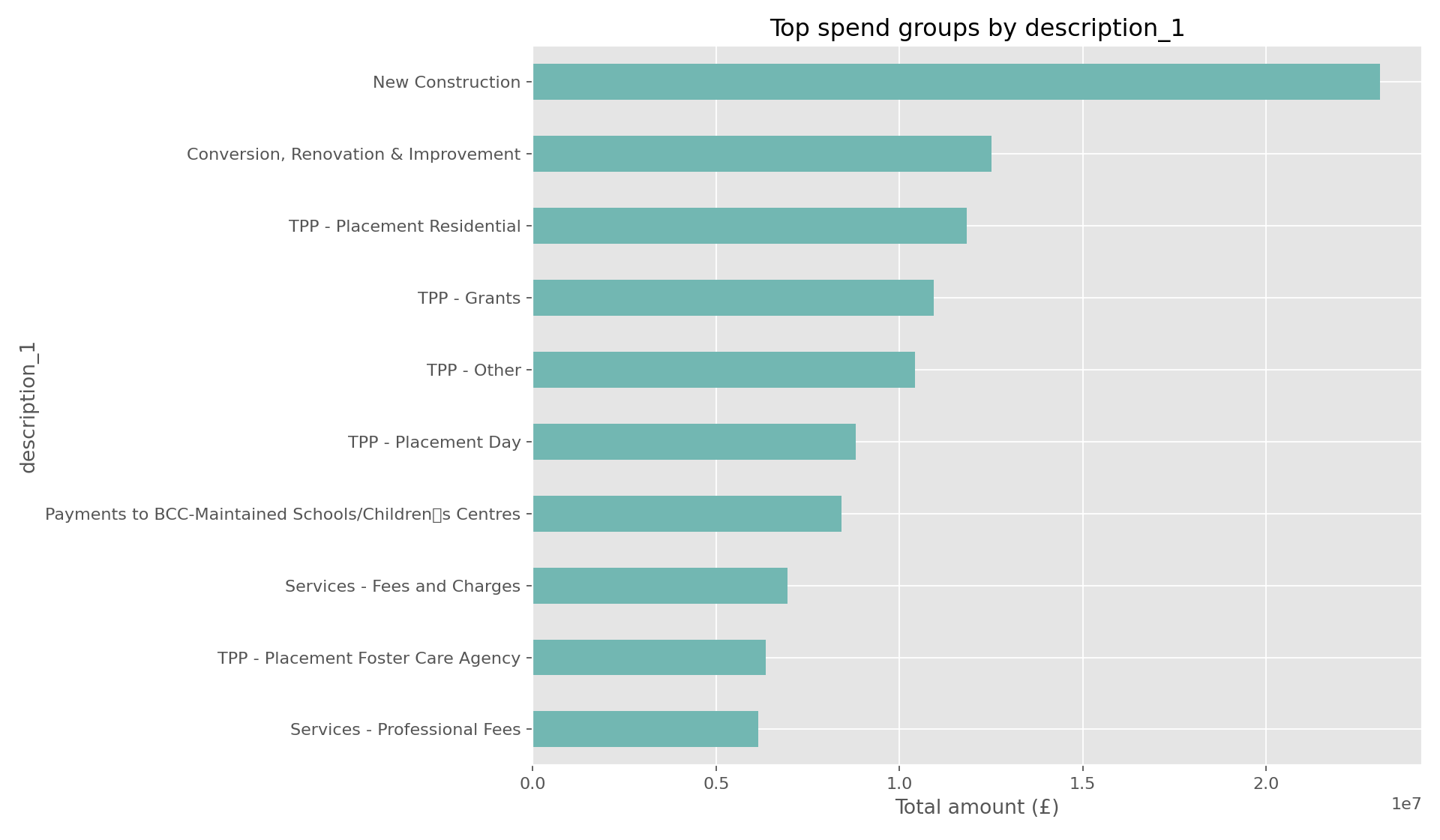

2. Spend categories and program patterns

The description_1 and description_2 fields provide a workable view of spend categories, programs, or departmental activity.

Among the largest groups by amount were:

- New Construction

- Conversion, Renovation & Improvement

- TPP - Placement Residential

- TPP - Grants

- Services - Fees and Charges

- TPP - Placement Foster Care Agency

This helps frame the project not just as payment analysis, but as a category-level review of where resources are concentrated.

3. Repeated payment patterns

Repeated values are not evidence of error by themselves, but they are very useful review candidates.

The analysis found:

- 1,147 groups with the same supplier + amount + payment date

- 4,152 rows inside those repeated groups

- 925 groups with the same transaction number + supplier

- 4,186 rows inside those groups

In practice, these patterns may reflect:

- valid recurring payments

- split lines under one process

- payment batches

- or cases worth a closer look for duplicate or fragmented payment review

4. Supplier-relative outliers

Looking only at the largest payments in the full dataset is not enough. A more useful audit view compares each transaction to the normal pattern of that supplier.

This approach surfaced notable outliers in suppliers such as:

- Jeff Way Construction Ltd

- Maples

- Oasis Support Ltd

- Constellia Public Limited

- REDACTED

This is a strong example of why supplier-relative analytics can add more value than global ranking alone.

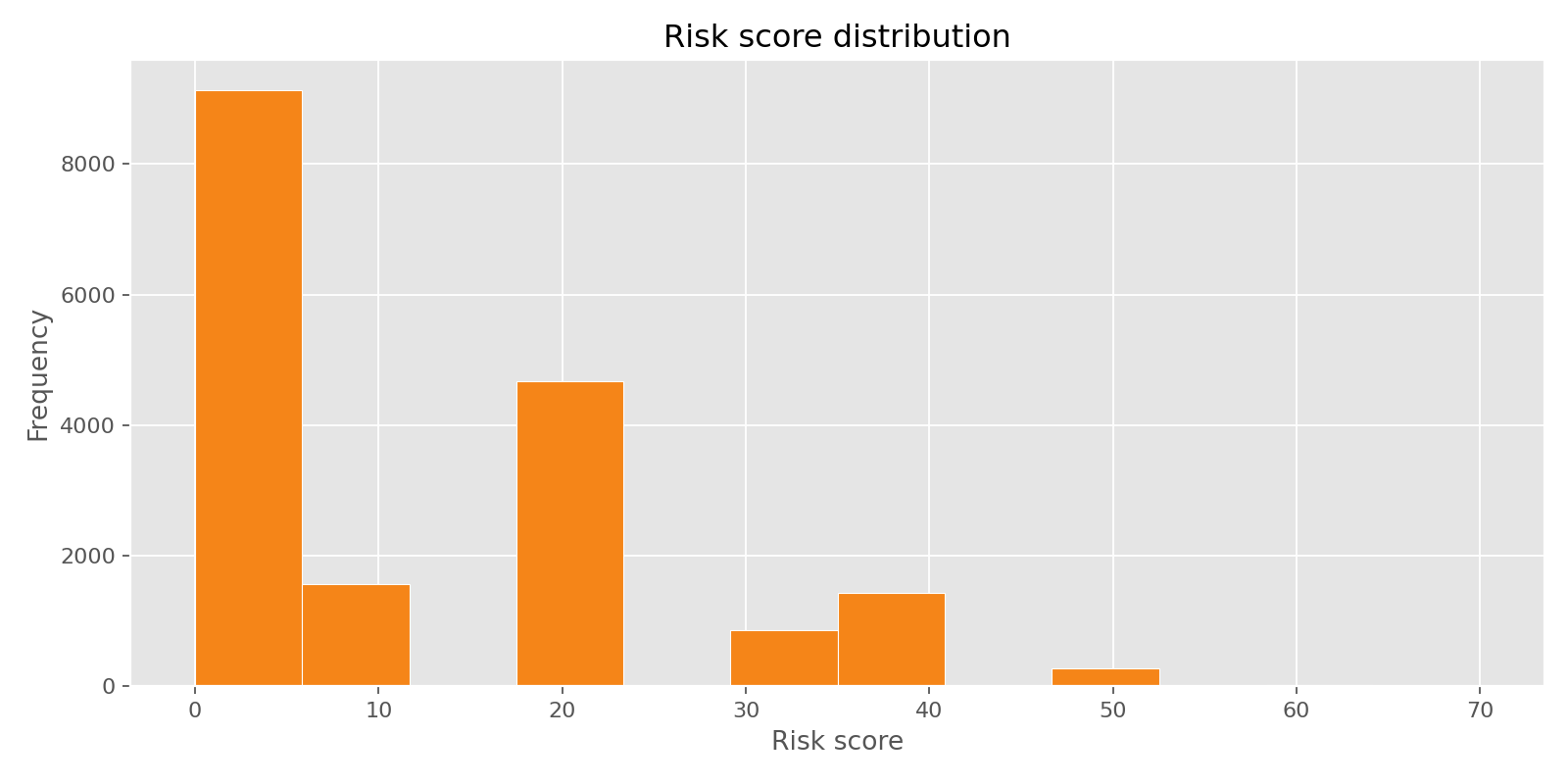

5. Review prioritization with a risk score

A rules-based score was built to create a review queue. The scoring considered flags such as:

- very large absolute amounts

- unusually large amounts relative to supplier history

- repeated supplier + amount + date combinations

- repeated transaction number + supplier combinations

- month-end timing

- redacted supplier names

This produced a small high-priority review set:

- 36 rows with risk score >= 60

- around 0.2% of the cleaned dataset

That is useful because it creates a manageable set of transactions for deeper review instead of applying the same attention to every row.

Why this project matters

This project is a good example of how data analytics can support audit and accounting work in a practical way. It does not depend on a complex black-box model. Instead, it combines:

- real public data

- clear cleaning logic

- supplier and category analysis

- repeated payment checks

- outlier detection

- explainable risk prioritization

That makes it well aligned with audit-oriented work where traceability, interpretability, and reviewability matter.